#Modular Robotics Market Trends

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr’s reach among the 26-to-35-year-olds in the US is 11%.

Text

How are Modular Robotics Systems Revolutionizing Factory Operations?

The ballooning utilization of collaborative modular robotics systems is one of the biggest factors responsible for the expansion of the global modular robotics market. Cobots, as they are popularly called, are revolutionizing robot and human relationships in the logistics and manufacturing industries. These systems allow operators to directly provide parts and components to robots for performing the rest of the operation, which leads to reduced requirement for floor space, lower costs, and shorter process time.

Additionally, the highly versatile nature of these systems allows them to perform various tasks and operations with the help of several suitable end-effectors. In the logistics industry, cobots are used for inspecting fragile goods and transporting loads and machine parts. Because of these reasons, the sales of collaborative modular robotics systems are rising rapidly across the world. Besides this, the growing requirement for automation in the manufacturing industry is also fueling the demand for these robots around the world.

Due to the aforementioned factors, the modular robotics market is growing rapidly all over the world. The valuation of the market is predicted to rise from $5.6 billion to $15.1 billion from 2019 to 2030. Furthermore, the market is expected to progress at a CAGR of 9.9% between 2020 and 2030. Depending on robot type, the market is categorized into cartesian modular robots, articulated modular robotics systems, SCARA modular robotics systems, parallel modular robots, and collaborative modular robots.

Out of these, the articulated modular robotics systems category recorded the highest growth in the market in the past years and this trend is likely to continue in the coming years as well. This would be due to the large-scale usage of these robots for handling and managing heavy automotive components and parts in the automotive industry. In addition to this, these robots are extensively used for handling heavy metal parts and sheets in the metal and machinery industry.

The growing sales of these robots are boosting the demand for services, software, and hardware. Out of these, the demand for hardware will be the highest in the future, as per the forecast of the market research company, P&S Intelligence. Sensors, manipulators, driver modules, and controllers are the most commonly used types of hardware. Amongst these, the usage of controllers is currently the highest, because of the utilization of robot controllers in various industrial robots for accomplishing point-to-point repetitive tasks.

Geographically, the modular robotics market registered the highest growth in the Asia-Pacific (APAC) region in the years gone by. This was because of the huge investments that were made in automation in electricals, electronics, and automotive industries, particularly in countries such as India, China, and South Korea. In addition to this, the high usage of collaborative modular robotics systems by various manufacturers further propelled the advancement of the market in the region in the past.

Hence, it can be said with full surety that the sales of modular robotics systems would shoot-up all over the world in the forthcoming years, mainly because of the rising requirement for automation in various industries such as automotive, logistics, electricals, and electronics and also, in the manufacturing sector.

Source: P&S Intelligence

#Modular Robotics Market Share#Modular Robotics Market Size#Modular Robotics Market Growth#Modular Robotics Market Applications#Modular Robotics Market Trends

1 note

·

View note

Text

0 notes

Text

Trends and Forecasts in the Second Life Industrial Robot Market

The Second Life Industrial Robot MarketSecond Life Industrial Robot Market is rapidly expanding as businesses increasingly seek cost-effective automation solutions across manufacturing, logistics, and automotive sectors. These pre-owned, refurbished robots offer a budget-friendly alternative to new systems while delivering reliable performance and extended lifecycles. Growing trends include advanced refurbishing services, AI integration, and alignment with Industry 4.0 technologies, enhancing robot adaptability and efficiency. Despite challenges like standardization gaps, compatibility issues, and skilled labor shortages, the market benefits from rising demand driven by cost optimization and sustainability efforts. With ongoing innovations and a focus on circular economy practices, the second-life robot market is poised for significant growth and greater adoption worldwide.

Market Segmentation:

1. By End Use:

Industrial

Waste Recycling

Others

2. By Type of Refurbishment:

New Controller Technology

Others

3. By Region:

North America

Europe

Asia-Pacific

Rest of the World

Key Market Players

ABB

FANUC

IRS Robotics

Key Demand Drivers

Inexpensive Automation for Small and Medium Businesses: Because second-life robots drastically lower startup costs, automation is now affordable for manufacturers on a budget as well as small and mid-sized businesses (SMEs). This affordability is especially alluring in budget-conscious competitive industries and growing markets.

Goals for the Circular Economy and Sustainability: Businesses are adopting sustainable practices as a result of increased environmental awareness and more stringent e-waste rules. In line with circular economy concepts, refurbished robots prolong the useful life of current gear while lowering the load on landfills and conserving vital resources.

Improvements in Technology: Refurbished robots are becoming more versatile thanks to improved controller systems, AI integration, and machine learning applications. These improvements make older models more useful in high-precision settings and smart factories by enabling them to function on par with machines of the latest generation.

Market Challenges

Absence of Standardized Procedures for Renovation: Variations in robot safety, dependability, and quality caused by inconsistent refurbishing procedures among vendors may worry end users and restrict further adoption.

Integration Difficulties: Connecting legacy systems to automation platforms, Industry 4.0 frameworks, or contemporary software environments may necessitate extensive adaptation. Potential customers may be turned off by these integration fees, which can cancel out any initial savings.

Lack of Skilled Workers: Industrial robot maintenance and repair require specialized technical knowledge. The consistency of refurbished equipment quality and the scalability of services can be affected by a shortage of qualified personnel.

Get your hands on this Sample Report to stay up-to-date on the latest developments in the Second Life Industrial Robot Market.

Gain deep information on Robotics and Automation Market. Click Here!

Future Outlook

Through 2030, the market for used industrial robots is anticipated to develop significantly due to the combined demands of sustainability and economic efficiency. The performance of reconditioned robots will continue to improve with the development of AI-enabled control systems and modular modifications, making them more and more feasible for high-end industrial applications. With the help of favorable government policies, growing SME automation, and fast industrialization, the Asia-Pacific area is expected to grow at the fastest rate. Because of its well-established robotics infrastructure and advanced refurbishing skills, North America is expected to continue to hold its dominant position.

Conclusion

With its perfect blend of cost, sustainability, and performance, the second life industrial robot market is becoming a vital part of the worldwide automation scene. Refurbished robots are turning out to be a valuable asset for contemporary industry as the need for intelligent, environmentally friendly, and scalable automation solutions increases. Even if there are still issues with standardization and integration today, industry cooperation, technical advancement, and training programs should help to lessen them over time. The market for second-life robots is positioned for long-term growth and change because to strong regional demand and growing environmental concern.

#Second Life Industrial Robot Market#Second Life Industrial Robot Industry#Second Life Industrial Robot Report#robotics#automation

0 notes

Text

Technology Behind Waterproof Connectors

In today’s interconnected world, the demand for reliable connectivity extends far beyond dry and controlled environments. From underwater equipment to outdoor lighting systems, waterproof connectors have become indispensable components in various industries. These connectors are engineered not just to transmit power or data, but also to withstand moisture, dust, extreme temperatures, and physical stress.Get more news about waterproof connector,you can vist our website!

What Are Waterproof Connectors?

Waterproof connectors are specially designed electrical connectors that can operate in environments where exposure to water or humidity is inevitable. These devices are sealed using various techniques—such as O-rings, gaskets, epoxy resin, or molded rubber—to prevent water ingress. They are categorized based on Ingress Protection (IP) ratings, with IP67 and IP68 being common standards for full waterproof capability.

Types of waterproof connectors range from circular and rectangular connectors to USB and Ethernet varieties, each tailored for specific voltage, current, and transmission needs.

Applications Across Industries

The versatility of waterproof connectors makes them essential across a wide spectrum of applications. In marine engineering, they are used to power underwater robots and sonar systems. In renewable energy, waterproof connectors ensure the safe transmission of power from solar panels and wind turbines, often exposed to harsh weather conditions.

Construction equipment, outdoor surveillance systems, LED lighting, transportation infrastructure, and even wearable medical devices frequently rely on these robust connectors to maintain reliability in dynamic or outdoor environments.

Design and Material Considerations

What separates a waterproof connector from a traditional one is not just the external seal but also the careful selection of materials. Housing is often made from high-performance thermoplastics, stainless steel, or aluminum alloy to provide mechanical strength and corrosion resistance. Contact points are gold or nickel-plated to enhance conductivity and prevent oxidation.

In addition, ergonomic design matters. Connectors may feature secure locking mechanisms such as bayonet, screw-thread, or push-pull designs to prevent accidental disconnections during operation or maintenance.

Technological Innovation and Trends

As industries continue to innovate, so too do the demands placed on waterproof connectors. The latest designs are not only compact and lighter but also offer improved data transmission speeds and higher voltage capacities. Smart connectors, equipped with built-in diagnostics or wireless monitoring features, are becoming increasingly common in industrial automation and military-grade equipment.

Environmental sustainability is another growing focus. Manufacturers are now exploring eco-friendly materials and modular designs that allow easier recycling and replacement, aligning with global environmental mandates.

Challenges and Market Outlook

Despite their benefits, waterproof connectors can be more expensive and complex to manufacture than their standard counterparts. Ensuring long-term sealing performance under pressure, temperature variation, and mechanical movement remains a technical challenge. Poor installation or degradation over time may still lead to leakage and failure.

However, the global market for waterproof connectors is projected to expand steadily over the next decade, driven by rising demand in smart cities, electric vehicles, offshore drilling, and the growing IoT infrastructure.

Conclusion

Whether submerged in water, battered by storms, or embedded in rugged terrain, waterproof connectors serve as silent yet critical lifelines that power modern infrastructure and innovation. Their evolution reflects the broader shift toward durable, intelligent, and sustainable technology solutions—connecting not only devices, but the future itself.

0 notes

Text

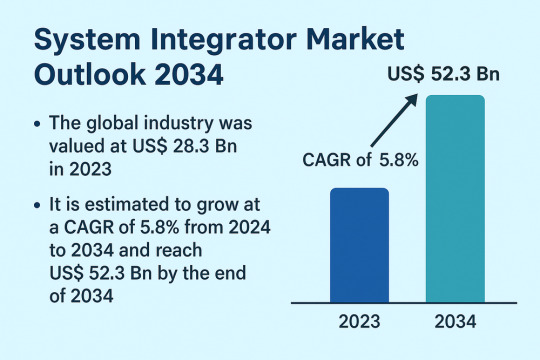

Automation and Integration Needs Power Robust Growth in System Integrator Market

The global System Integrator Market is poised for significant growth, projected to rise from US$ 28.3 Bn in 2023 to US$ 52.3 Bn by 2034, growing at a CAGR of 5.8% from 2024 to 2034. This growth is driven by the widespread adoption of industrial robots, technological advancements, and a pressing need among businesses to optimize operational efficiencies through connected systems.

System integrators play a pivotal role in designing, implementing, and maintaining integrated solutions that bring together hardware, software, and consulting services. These services support organizations in unifying internal and external systems, such as SCADA, HMI, MES, PLC, and IIoT, to enable seamless data flow and system interoperability.

Market Drivers & Trends: One of the primary market drivers is the rise in adoption of industrial robots. As industries accelerate automation, robotic system integrators have become vital in delivering customized, scalable, and high-performing solutions tailored to complex manufacturing needs.

Another major catalyst is the surge in technological advancements. Integrators are deploying cloud-based tools and platforms that provide real-time data insights, improve developer productivity, and support hybrid architectures. The increasing use of Artificial Intelligence (AI), Machine Learning (ML), and Internet of Things (IoT) in integration solutions is fostering innovation and growth.

Latest Market Trends

Several emerging trends are shaping the system integrator landscape:

Cloud modernization platforms such as IBM’s Z and Cloud Modernization Center are enabling businesses to accelerate the transition to hybrid cloud environments.

Modular automation platforms are gaining popularity, allowing companies to rapidly deploy and scale integration solutions across multiple industry verticals.

Edge computing and cybersecurity solutions are increasingly being integrated to support secure, real-time decision-making on the production floor.

Digital hubs and scalable workflow engines are being adopted by integrators to support multi-specialty applications with high adaptability.

Key Players and Industry Leaders

The system integrator market is characterized by a strong mix of global leaders and regional specialists. Key players include:

ATS Corporation

Avanceon

Avid Solutions

Brock Solutions

JR Automation

MAVERICK Technologies, LLC

Burrow Global, LLC

BW Design Group

John Wood Group PLC

TESCO CONTROLS

These companies are actively investing in next-generation technologies, enhancing their product portfolios, and pursuing strategic acquisitions to strengthen market presence. For instance, in July 2023, ATS Corporation acquired Yazzoom BV, a Belgian AI and ML solutions provider, expanding their capabilities in smart manufacturing.

Recent Developments

Olympus Corporation launched the EASYSUITE ES-IP system in July 2023 in the U.S., offering advanced visualization and integration solutions for procedure rooms.

IBM introduced key updates in 2021 and 2022 to streamline mission-critical application modernization using cloud services and hybrid IT strategies.

Asia-Pacific companies have led the charge in deploying advanced integrated systems, reflecting the rapid industrial digitization in countries such as China, Japan, and South Korea.

Market Opportunities

Opportunities abound in both mature and emerging markets:

Smart factories and Industry 4.0 transformation offer immense potential for integrators to offer comprehensive solutions tailored to real-time analytics, predictive maintenance, and remote monitoring.

Government-led infrastructure modernization projects, particularly in Asia and the Middle East, are increasing demand for integrated control systems and plant asset management solutions.

The energy transition movement, including renewables and electrification of industrial processes, requires new types of integration across decentralized assets.

Future Outlook

As industries pursue digital transformation, the role of system integrators will evolve from traditional project implementers to long-term strategic partners. The future will see increasing demand for intelligent automation, cross-domain expertise, and real-time adaptive solutions. Vendors who can provide holistic, secure, and scalable services will dominate the landscape.

With continued advancements in AI, IoT, and robotics, the system integrator market will continue to thrive, transforming operations across diverse sectors, from automotive and food & beverages to oil & gas and pharmaceuticals.

Review critical insights and findings from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=82550

Market Segmentation

The market is segmented based on offering, technology, and end-use industry.

By Offering:

Hardware

Software

Service (Consulting, Design, Installation)

By Technology:

Human-Machine Interface (HMI)

Supervisory Control and Data Acquisition (SCADA)

Manufacturing Execution System (MES)

Functional Safety System

Machine Vision

Industrial Robotics

Industrial PC

Industrial Internet of Things (IIoT)

Machine Condition Monitoring

Plant Asset Management

Distributed Control System (DCS)

Programmable Logic Controller (PLC)

By End-use Industry:

Oil & Gas

Chemical & Petrochemical

Food & Beverages

Automotive

Energy & Power

Pharmaceutical

Pulp & Paper

Aerospace

Electronics

Metals & Mining

Others

Regional Insights

Asia Pacific leads the global system integrator market, holding the largest market share in 2023. This leadership is attributed to:

Rapid industrialization and digital transformation in China, Japan, and India.

Strong investments in smart manufacturing and Industry 4.0 initiatives.

Government support for infrastructure modernization, especially through Smart City programs and cybersecure IT frameworks.

North America and Europe also show strong demand, driven by the presence of established manufacturing facilities and a robust focus on sustainable operations and green automation.

Why Buy This Report?

Comprehensive Market Analysis: Deep insights into market size, share, and growth across all major segments and geographies.

Detailed Competitive Landscape: Profiles of leading companies with analysis of their strategy, product offerings, and key financials.

Actionable Intelligence: Understand technological trends, regulatory developments, and investment opportunities.

Forecast-Based Strategy: Develop long-term strategic plans using data-driven forecasts up to 2034.

Frequently Asked Questions (FAQs)

1. What is the projected value of the system integrator market by 2034? The global system integrator market is projected to reach US$ 52.3 Bn by 2034.

2. What is the current CAGR for the forecast period 2024–2034? The market is anticipated to grow at a CAGR of 5.8% during the forecast period.

3. Which region holds the largest market share? Asia Pacific dominated the global market in 2023 and is expected to continue leading due to rapid industrialization and technology adoption.

4. What are the key growth drivers? Key drivers include the rise in adoption of industrial robots and continuous advancements in integration technologies like IIoT, AI, and cloud platforms.

5. Who are the major players in the system integrator market? Prominent players include ATS Corporation, JR Automation, Brock Solutions, MAVERICK Technologies, and Control Associates, Inc.

6. Which industries are adopting system integrator services the most? High adoption is seen in industries such as automotive, oil & gas, food & beverages, pharmaceuticals, and electronics.

Explore Latest Research Reports by Transparency Market Research:

Multi-Mode Chipset Market: https://www.transparencymarketresearch.com/multi-mode-chipset-market.html

Accelerometer Market: https://www.transparencymarketresearch.com/accelerometer-market.html

Luminaire and Lighting Control Market: https://www.transparencymarketresearch.com/luminaire-lighting-control-market.html

Advanced Marine Power Supply Market: https://www.transparencymarketresearch.com/advanced-marine-power-supply-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Vertical Farming Market to Hit $13.7 Billion by 2029 Driven by AI and Sustainability

The Vertical Farming Market is poised for exponential growth, forecasted to increase from approximately USD 5.6 billion in 2024 to USD 13.7 billion by 2029, growing at a compound annual growth rate (CAGR) of 19.7%. This transformation is being driven by urbanization, increasing food demand, water scarcity, and technological innovations including artificial intelligence (AI), LED lighting, and hydroponic systems.

To Get Free Sample Report: https://www.datamintelligence.com/download-sample/vertical-farming-market

Market Drivers and Growth Opportunities

Scarcity of Arable Land and Water Vertical farming systems require up to 97% less water and significantly less land than traditional farming, making them ideal for densely populated cities and regions suffering from water scarcity.

Integration of AI and Automation AI is revolutionizing vertical farming by enabling predictive analytics, automation of nutrient delivery, environmental control, and yield optimization. Coupled with IoT and sensors, farms can operate efficiently with minimal human input.

Year-Round Production and Urban Scalability Controlled environment agriculture allows year-round production regardless of climate conditions. This is especially crucial in urban areas where local food production can reduce dependency on external supply chains and transportation.

Rising Demand for Clean, Pesticide-Free Produce Health-conscious consumers are driving demand for fresh, pesticide-free food. Vertical farming offers a solution with clean growing environments that eliminate the need for chemical treatments.

Government Incentives and Policy Support Supportive policies in both developed and developing countries are fostering investment and research in sustainable agricultural practices, including vertical farming.

U.S. Market Insights

The United States is one of the leading adopters of vertical farming technology. In urban food deserts regions with limited access to fresh food small and modular farms are addressing local needs. For example, projects in cities like Houston, Phoenix, and Mesa are creating access to greens using hydroponics and aeroponics.

Energy use remains a major challenge, as climate-controlled farms consume high levels of electricity. However, innovators are mitigating this through renewable energy integration and partnerships with local energy providers. Furthermore, advanced LED lighting is being optimized for energy efficiency.

Despite some high-profile vertical farm companies declaring bankruptcy due to overexpansion or unprofitable scale, many small and mid-size operators are succeeding with localized, efficient models. Companies like Bowery Farming are providing produce to major retailers including Walmart and Whole Foods, supported by automation and AI tools that streamline farm management.

Startups like True Garden are demonstrating profitability with container-based models, producing thousands of pounds of greens each month while using 90–98% less water than traditional farms.

Japan Market Trends

Japan’s vertical farming industry is expanding rapidly, driven by the need for domestic food production and sustainability. Indoor farms, known as "vegetable factories," are increasingly integrated into urban environments. The vertical farming market in Japan was valued at USD 402 million in 2024 and is projected to reach USD 879 million by 2033, with a CAGR of 9.1%.

Robotics, biosciences, and AI are at the core of Japan's vertical farming technology. Companies like Spread are leveraging cloud-based farm management systems to distribute greens to thousands of retail stores. The cultural alignment with sustainability, minimal waste, and urban efficiency positions Japan as a key global influencer in vertical farming.

Government funding and corporate investment are further accelerating growth, particularly in the development of fully automated farming systems that reduce reliance on human labor.

Global Market Landscape

The Asia-Pacific region, beyond Japan, is also witnessing notable growth. In 2023, the market was valued at USD 1.77 billion and is projected to reach USD 7.04 billion by 2030 at a CAGR of 21.8%. Countries such as Singapore, South Korea, and China are investing heavily in vertical farming for urban food security.

Hydroponics is currently the dominant method due to its water efficiency and scalability. Aeroponics is gaining momentum, especially in Japan and parts of Europe, due to its superior nutrient delivery and root oxygenation.

Investment Opportunities

Vertical farming is attracting venture capital across multiple fronts:

Automation and AI: Investors are prioritizing platforms that use AI to manage farm ecosystems in real-time.

Container and Modular Farms: Scalable, transportable farms offer a solution for urban redevelopment and rural supply gaps.

Premium Crop Segments: High-value crops like microgreens, strawberries, and herbs offer better margins for vertical farmers.

Food Security Projects: Urban governments and non-profits are partnering with startups to launch vertical farms in underserved neighborhoods.

Get the Demo Full Report : https://www.datamintelligence.com/enquiry/vertical-farming-market

Industry Challenges

High Energy and Infrastructure Costs Energy-intensive systems for lighting, heating, and environmental control present cost challenges. Co-locating farms with renewable energy sources is a potential solution.

Scalability and Profitability Balance Large-scale operations often struggle with profitability, whereas smaller localized farms show better financial performance and community impact.

Supply Chain and Distribution Ensuring freshness and shelf life, especially for leafy greens, requires efficient local distribution networks.

Conclusion

The vertical farming market is on a transformative path. Innovations in AI, hydroponics, and sustainable lighting are enabling farms to flourish in environments previously unsuitable for agriculture. While energy consumption and initial investment remain hurdles, the long-term benefits of local food production, water savings, and food security are positioning vertical farming as a central player in the future of agriculture. With leadership from the U.S. and Japan, and rapid growth in the Asia-Pacific region, vertical farming is no longer experimental it is becoming essential.

0 notes

Text

Pedicle Screw Systems Market : Size, Trends, and Growth Analysis 2032

The Pedicle Screw Systems Market was valued at US$ 1,998.90 million in 2024 and is projected to grow at a CAGR of 5.90% from 2025 to 2032. The increasing global burden of spinal disorders, coupled with advances in minimally invasive surgical technologies, is fueling the demand for robust spinal fixation systems. Among these, pedicle screw systems have become the cornerstone of spinal fusion and deformity correction procedures, offering unmatched structural support and surgical outcomes.

What Are Pedicle Screw Systems?

Pedicle screw systems are specialized orthopedic implants used in spinal stabilization procedures, particularly spinal fusion surgeries. These systems consist of screws that are inserted into the pedicles — the cylindrical bony projections off the back of each vertebra. Once secured, the screws are connected using rods, hooks, or plates to form a rigid frame that stabilizes the spine, allowing vertebrae to fuse together over time.

This system is designed to limit movement in the affected spinal segment, thereby promoting healing and reducing pain caused by spinal instability, deformities, or degenerative conditions.

Key Market Drivers

1. Rising Incidence of Spinal Disorders

Conditions such as scoliosis, spinal stenosis, spondylolisthesis, herniated discs, and traumatic spinal injuries are on the rise due to aging populations, sedentary lifestyles, and increased road traffic accidents. These disorders often necessitate surgical intervention involving pedicle screw systems to restore spinal alignment and stability.

2. Growth in Minimally Invasive Spine Surgery (MISS)

Minimally invasive techniques are revolutionizing spinal surgeries by offering reduced recovery times, less blood loss, and smaller incisions. Many modern pedicle screw systems are specifically designed for MISS, allowing surgeons to perform precise screw placement under fluoroscopic or robotic guidance.

3. Technological Advancements in Implant Design

Manufacturers are innovating with biocompatible materials (like titanium and PEEK), improved thread designs, and cannulated screws for percutaneous placement. Customizable and modular systems are also gaining traction, allowing surgeons greater flexibility in addressing patient-specific anatomical challenges.

4. Increased Surgical Volumes Worldwide

With greater access to healthcare and rising awareness of surgical solutions for chronic back pain, both elective and trauma-related spinal surgeries are increasing globally. This directly boosts demand for pedicle screw systems as standard-of-care instrumentation in spine stabilization.

5. Robotics and Navigation Technology Integration

The integration of robot-assisted surgical platforms and 3D navigation systems has elevated the accuracy of pedicle screw placement. These technologies reduce the risk of neurological damage and post-operative complications, further enhancing the appeal of pedicle screw-based surgeries.

Application Segmentation

Degenerative Disc Disease: A common cause of lower back pain, often requiring fusion to restore disc height and eliminate motion between vertebrae.

Spinal Trauma and Fractures: Pedicle screws provide immediate stabilization in cases of vertebral fractures due to accidents or falls.

Scoliosis and Spinal Deformities: Used to correct and maintain spinal alignment in congenital, idiopathic, or neuromuscular scoliosis cases.

Spinal Tumors and Infections: When surgical excision leads to destabilization, pedicle screws help support the remaining spinal structure.

Revision Surgeries: In cases where previous surgeries have failed, robust fixation systems like pedicle screws are often re-employed.

Product Insights

Monoaxial Pedicle Screws: Offer rigid fixation, used in deformity correction when high stability is required.

Polyaxial Pedicle Screws: Allow multidirectional movement, preferred in procedures requiring anatomical alignment flexibility.

Cannulated Screws: Enable percutaneous insertion, ideal for minimally invasive surgeries.

Expandable Screws: Designed to increase anchorage in patients with osteoporotic bone, improving fixation in the elderly.

Regional Analysis

North America

Holds the largest share due to high surgical volumes, rapid adoption of novel technologies, and strong presence of market leaders. The U.S. leads in spine surgery rates, supported by advanced hospital infrastructure.

Europe

Second-largest market driven by growing aging populations, especially in countries like Germany, France, and the UK. Reimbursement support and a skilled healthcare workforce boost market growth.

Asia-Pacific

Fastest-growing region owing to increasing healthcare access, rising spinal disorder prevalence, and a surge in medical tourism, particularly in countries like India, China, and South Korea.

Latin America & Middle East and Africa (MEA)

Emerging markets where investment in healthcare infrastructure and growing awareness about surgical treatment options are expanding the scope for pedicle screw system adoption.

Key Market Players

Medtronic PLC

A global leader in spinal implants, Medtronic offers a comprehensive suite of pedicle screw systems under its Spinal & Biologics division, with a focus on minimally invasive and robotic-compatible technologies.

DePuy Synthes (Johnson & Johnson)

Offers advanced spinal fixation systems known for modularity and ease of use, supported by the company’s global distribution network and surgeon training programs.

Stryker Corporation

Renowned for innovative product designs and integration with its MAKO robotic platform, enhancing precision in screw placement and surgical outcomes.

Zimmer Biomet

Delivers spinal hardware systems with a focus on patient-centric solutions, including expandable and MIS-friendly pedicle screw products.

Globus Medical Inc.

A strong innovator in spinal surgery technologies, Globus is investing in robotic guidance and next-gen pedicle screw platforms.

NuVasive Inc.

A pioneer in lateral spine surgery techniques, NuVasive develops highly specialized pedicle screw systems aligned with MISS protocols.

Orthofix Medical Inc.

Focused on fusion and non-fusion spinal solutions, Orthofix’s systems are often used in trauma, deformity, and complex spinal reconstruction cases.

Market Trends

Patient-Specific Implants: Custom 3D-printed pedicle screws and guides are being developed based on patient imaging data, increasing surgical accuracy and fit.

Osteoporotic Solutions: With aging demographics, there is a rising focus on screw designs that improve purchase in brittle bone, such as expandable and cement-augmented screws.

Sustainability and Biocompatibility: A shift toward recyclable, hypoallergenic materials and coatings that reduce inflammation and improve long-term outcomes.

Smart Implants: Future potential lies in sensor-embedded screws that monitor healing progress or implant stress post-operatively.

Browse more Report:

Instrumentation Sterilization Containers Market

Infectious Enteritis Treatment Market

High-Integrity Pressure Protection System Market

High Temperature Overhead Conductor Market

Flowable Hemostats Market

0 notes

Text

Modular Hall Effect Sensors Market: Future Growth of the Semiconductor Sector, 2025–2032

MARKET INSIGHTS

The global Modular Hall Effect Sensors Market size was valued at US$ 834 million in 2024 and is projected to reach US$ 1.34 billion by 2032, at a CAGR of 7.1% during the forecast period 2025-2032. The U.S. market accounted for 32% of global revenue in 2024, while China is expected to witness the highest growth rate at 7.8% CAGR through 2032.

Modular Hall Effect sensors are compact, overmolded devices that detect magnetic fields with IP67-rated protection. These sensors separate the magnetic target from enclosed electronics, enabling space-efficient installations in demanding environments. They offer both analog and digital output options, making them versatile for position sensing, speed detection, and current measurement applications across industries.

The market growth is driven by increasing automation in manufacturing and rising electric vehicle production, where these sensors enable precise motor control. Furthermore, advancements in Industry 4.0 technologies and growing adoption in consumer electronics for touchless interfaces are expanding application horizons. Key players like Allegro MicroSystems and Texas Instruments are introducing energy-efficient variants with integrated signal conditioning, addressing the need for smarter IoT-enabled solutions.

MARKET DYNAMICS

MARKET DRIVERS

Growing Adoption in Automotive Applications Fuels Market Expansion

The automotive industry’s increasing reliance on modular Hall effect sensors is a primary driver for market growth. These sensors are critical for position sensing in throttle control, gear shift detection, and braking systems in modern vehicles. With the automotive sector accounting for over 35% of global Hall effect sensor demand, the transition toward electric vehicles (EVs) and advanced driver-assistance systems (ADAS) creates substantial opportunities. The integration of these sensors in brushless DC motors for EV powertrains, where they offer high reliability in harsh environments, is particularly noteworthy. Recent technological advancements have enhanced their ability to operate in temperature ranges from -40°C to 150°C, making them indispensable for automotive applications.

Industrial Automation Boom Accelerates Demand

Industrial automation represents another significant growth avenue, with modular Hall effect sensors finding extensive use in motor controls, robotics, and conveyor systems. The global industrial automation market is projected to grow at nearly 9% CAGR through 2030, creating parallel demand for precision sensing solutions. These sensors enable non-contact position detection in harsh industrial environments where traditional mechanical switches fail. Their modular design with IP67-rated housings provides robust protection against dust and moisture, a critical requirement in manufacturing facilities. Furthermore, Industry 4.0 initiatives are driving the adoption of smart sensors with digital outputs that can interface directly with IoT systems, creating new integration possibilities.

➤ An analysis of production data shows that industrial applications now account for approximately 28% of modular Hall effect sensor deployments, with particularly strong uptake in packaging machinery and CNC equipment.

The trend toward miniaturization in consumer electronics also presents significant growth potential. As devices become smaller, modular Hall effect sensors offer compact solutions for lid position detection in laptops and foldable smartphones, with some models now measuring less than 2mm x 2mm.

MARKET CHALLENGES

Intense Price Competition from Alternative Technologies

While modular Hall effect sensors offer distinct advantages, they face mounting competition from alternative sensing technologies like magnetoresistive (MR) and giant magnetoresistive (GMR) sensors. These alternatives often provide higher sensitivity and better signal-to-noise ratios in certain applications, putting pressure on Hall sensor manufacturers to differentiate their offerings. In price-sensitive markets such as consumer electronics, this competition frequently leads to margin erosion, with some sensor prices declining by approximately 15% over the past three years. Maintaining profitability while meeting the demand for cost reductions remains an ongoing challenge for major players.

Other Challenges

Supply Chain Vulnerabilities The semiconductor shortage impacts have revealed vulnerabilities in the sensor supply chain, particularly for specialized packaging materials. Lead times for certain sensor components have extended to 26 weeks in some cases, disrupting production schedules.

Technical Limitations Achieving sub-micron position resolution remains technically challenging for standard Hall effect designs, limiting their adoption in ultra-high precision applications compared to optical encoders.

MARKET RESTRAINTS

Design Complexity in High-Temperature Applications

While modular Hall effect sensors perform well in standard industrial environments, their application in extreme conditions presents design challenges. Operation above 150°C requires specialized materials and packaging techniques that can increase unit costs by 30-40%. This temperature limitation restricts their use in certain aerospace and oil/gas applications where environments routinely exceed these thresholds. The thermal drift characteristics of Hall elements also necessitate sophisticated compensation circuits, adding to system complexity and BOM costs.

Additionally, the need for precise magnetic field calibration in production creates yield challenges, with typical manufacturing tolerances requiring adjustments to ±1% or better for critical applications. These factors collectively restrain broader market adoption in some specialized segments.

MARKET OPPORTUNITIES

Emerging Medical Applications Present Significant Growth Potential

The medical device sector represents a high-growth opportunity, with modular Hall effect sensors finding new applications in surgical robotics, drug delivery systems, and implantable devices. The medical sensors market is projected to exceed $20 billion by 2027, creating substantial demand for reliable position sensing solutions. Recent innovations include contactless sensing for MRI-compatible equipment and miniature sensors for insulin pump mechanisms. The sterilization compatibility of properly packaged modular sensors makes them particularly attractive for single-use medical devices.

Furthermore, the development of ultra-low power Hall sensors consuming less than 10μA enables new battery-powered wearable applications with multi-year operational life, opening additional market segments. Strategic partnerships between sensor manufacturers and medical OEMs are accelerating the development of application-specific solutions.

MODULAR HALL EFFECT SENSORS MARKET TRENDS

Shift Towards Compact, High-Performance Sensing Solutions Drives Market Growth

The global Modular Hall Effect Sensors market, valued at $XX million in 2024, is experiencing robust expansion due to increasing demand for compact and reliable sensing solutions in industrial and automotive applications. These sensors, known for their IP67-rated durability and separation of magnetic targets from enclosed electronics, offer significant advantages in space-constrained installations. The automotive sector alone accounts for over 30% of total sensor demand, driven by the need for precise position detection in electric power steering and transmission systems. As industries continue miniaturizing components while requiring higher precision, modular Hall effect sensors are becoming the technology of choice for engineers worldwide.

Other Trends

Industrial Automation Revolution

The fourth industrial revolution is accelerating adoption across manufacturing sectors, with modular Hall effect sensors playing a critical role in Industry 4.0 implementations. These contactless sensors enable precise speed measurement in conveyor systems with an accuracy margin of ±1%, while their modular design allows easy integration into existing automated workflows. The global industrial automation market’s projected CAGR of 9.3% through 2032 directly correlates with increasing sensor deployments in robotic assembly lines and smart factory environments.

Advancements in Material Science and Chip Design

Recent breakthroughs in semiconductor materials and 3D packaging technologies are enabling sensor manufacturers to develop products with 30% higher sensitivity compared to previous generations. Leading manufacturers are now incorporating graphene-based elements and advanced ferromagnetic alloys that maintain stability across extreme temperature ranges from -40°C to 150°C. These innovations are particularly crucial for aerospace applications where sensors must perform reliably in both stratospheric cold and engine compartment heat. Digital output variants now dominate new product launches, representing 58% of 2024 modular Hall sensor introductions due to their compatibility with modern IoT ecosystems.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Leadership

The global modular Hall Effect sensors market exhibits a moderately consolidated competition structure, where established electronic component manufacturers compete with specialized sensor providers. Sensata Technologies leads the segment with an estimated 18% revenue share in 2024, leveraging its diversified industrial sensor portfolio and strong OEM relationships in the automotive sector.

Texas Instruments and Allegro MicroSystems collectively hold approximately 25% market share, driven by their advanced semiconductor expertise and vertically integrated production capabilities. These companies continue to dominate due to their ability to offer customized solutions for high-growth applications such as electric vehicles and Industry 4.0 automation systems.

While traditional players maintain strong positions, emerging competitors like Melexis are disrupting the market through innovative packaging technologies and miniaturized sensor designs. The Belgium-based company recently launched its third-generation Hall Effect ICs, specifically optimized for space-constrained medical devices and wearables.

The supplier ecosystem is witnessing increased M&A activity as manufacturers seek to consolidate expertise. Littelfuse’s 2023 acquisition of C&K Components exemplifies this trend, enhancing their position in ruggedized industrial sensors. Similarly, Rohm Semiconductor expanded its European footprint through strategic partnerships with automotive Tier 1 suppliers.

List of Key Modular Hall Effect Sensor Companies Profiled

Sensata Technologies (U.S.)

Texas Instruments (U.S.)

Rohm Semiconductor (Japan)

Littelfuse (U.S.)

ZF Switches & Sensors (Germany)

Marposs (Italy)

Allegro MicroSystems (U.S.)

Lake Shore Cryotronics (U.S.)

Regal Components (Sweden)

Silicon Labs (U.S.)

Melexis (Belgium)

Segment Analysis:

By Type

Hall Switch Segment Leads the Market with Extensive Use in Position Sensing and Switching Applications

The market is segmented based on type into:

Hall Switch

Subtypes: Unipolar, Bipolar, and Omnipolar

Linear Hall Sensor

Subtypes: Analog Output and Digital Output

Others

By Application

Automotive Segment Dominates Due to Increasing Adoption in Position Detection and Current Sensing Applications

The market is segmented based on application into:

Consumer Electronics

Automotive

Aerospace

Medical

Industrial

By Functionality

Position Sensing Segment Holds Major Share with Growing Demand Across Industries

The market is segmented based on functionality into:

Position Sensing

Current Sensing

Speed Detection

Others

By Output

Analog Output Segment Maintains Strong Position in Various Measurement Applications

The market is segmented based on output into:

Analog Output

Digital Output

Subtypes: Pulse Width Modulation (PWM), I2C, and SPI

Others

Regional Analysis: Modular Hall Effect Sensors Market

North America The North American market remains a key revenue generator for modular Hall effect sensors, driven by strong automotive and industrial automation demand. The U.S. accounts for over 60% of the regional market value, benefiting from heavy investments in electric vehicle manufacturing and smart factory initiatives. Recent technological advancements by market leaders like Allegro MicroSystems and Texas Instruments have strengthened product offerings in high-temperature and high-precision applications. However, pricing pressures from Asian manufacturers pose a challenge to domestic producers. The Canadian market shows steady growth, particularly in aerospace and medical equipment segments where reliability is paramount.

Europe Europe’s market is characterized by stringent quality standards and innovation-driven demand, particularly in automotive and industrial sectors. Germany leads adoption with its robust manufacturing base, while Nordic countries demonstrate increasing usage in renewable energy systems. The Hall Switch segment dominates due to its prevalence in automotive position sensing applications. European OEMs emphasize miniaturization and energy efficiency, creating opportunities for modular sensors with integrated signal processing. However, the transition to electric vehicles has temporarily disrupted traditional supply chains, causing suppliers to realign production capacities toward EV-specific sensor solutions.

Asia-Pacific Asia-Pacific represents the fastest-growing regional market, projected to capture over 45% of global demand by 2032. China’s dominance stems from massive electronics production and government-backed Industry 4.0 initiatives fueling industrial automation. Japanese manufacturers lead in high-precision applications like robotics, while South Korea sees strong demand from consumer electronics giants. The region witnesses intense price competition, with local players like ROHM Semiconductor gaining market share through cost-effective solutions. India emerges as a promising market with expanding automotive manufacturing and infrastructure modernization programs, though quality consistency remains a concern among buyers.

South America Market growth in South America remains moderate, constrained by economic instability and limited local manufacturing capabilities. Brazil accounts for nearly half the regional demand, primarily serving automotive and appliance industries. Cost sensitivity drives preference for basic Hall Switch models over advanced linear sensors. While foreign investments in Argentina’s industrial sector show potential, currency volatility discourages long-term commitments from major sensor suppliers. The aftermarket for sensor replacements presents steady opportunities, particularly in aging industrial equipment maintenance across the continent.

Middle East & Africa This region demonstrates uneven growth patterns, with Gulf Cooperation Council countries leading adoption in oil/gas and building automation applications. Israel’s thriving medical technology sector drives specialist demand for high-reliability sensors. South Africa serves as an industrial hub for sub-Saharan Africa, though infrastructure limitations hinder widespread sensor integration. The market sees increasing Chinese imports due to competitive pricing, while European suppliers maintain dominance in high-value industrial projects. Government initiatives to diversify economies toward manufacturing create long-term growth potential, albeit from a comparatively small base.

Report Scope

This market research report provides a comprehensive analysis of the global Modular Hall Effect Sensors market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD million in 2024 and is projected to reach USD million by 2032.

Segmentation Analysis: Detailed breakdown by product type (Hall Switch, Linear Hall Sensor), application (Consumer Electronics, Automotive, Aerospace, Medical, Industrial), and end-user industry to identify high-growth segments.

Regional Outlook: Insights into market performance across North America (USD million market size in U.S.), Europe, Asia-Pacific (China projected at USD million), Latin America, and Middle East & Africa.

Competitive Landscape: Profiles of leading market participants including Sensata Technologies, Texas Instruments, Allegro MicroSystems, and others holding approximately % market share in 2024.

Technology Trends & Innovation: Assessment of emerging sensor technologies, integration with IoT systems, and evolving industry standards for magnetic sensing applications.

Market Drivers & Restraints: Evaluation of factors including automotive electrification, industrial automation demand, along with supply chain constraints and material cost challenges.

Stakeholder Analysis: Strategic insights for sensor manufacturers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/global-video-sync-separator-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/silicon-rings-and-silicon-electrodes_17.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ceramic-bonding-tool-market-investments.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/coaxial-panels-market-challenges.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/oled-and-led-automotive-light-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/gas-cell-market-demand-for-ai-chips-in.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/digital-demodulator-ic-market-packaging.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/nano-micro-connector-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/single-mode-laser-diode-market-growth.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/silicon-rings-and-silicon-electrodes.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/battery-management-system-chip-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/scanning-slit-beam-profiler-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/atomic-oscillator-market-electronics.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/plastic-encapsulated-thermistor-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ceramic-bonding-tool-market-policy.html

0 notes

Text

A Deep Dive into Interface & Connectivity Semiconductors: Market Opportunities and Challenges

The rapid acceleration of digital transformation across industries has ushered in a critical dependence on robust data communication systems. At the heart of these systems lie interface and connectivity semiconductors, which serve as essential conduits for transferring data between integrated circuits, sensors, and peripheral devices. Whether it is automotive, consumer electronics, industrial automation, or telecommunications, the ability of devices to communicate effectively defines their functionality and performance. The significance of these semiconductors is steadily increasing as devices grow smarter, more connected, and more autonomous.

Connectivity demands are evolving in complexity and scope. Advanced applications require high-speed data transmission, low latency, signal integrity, and resilience against electromagnetic interference. The role of interface and connectivity semiconductors, therefore, is not just to bridge data paths but to ensure seamless, reliable communication under increasingly demanding conditions. As markets grow more competitive and consumer expectations rise, semiconductor manufacturers are tasked with not only meeting technical requirements but also innovating at the architectural level to stay ahead of the curve.

The Role of Interface & Connectivity Semiconductors

Interface and connectivity semiconductors provide the vital infrastructure that allows systems and subsystems within electronic devices to interact efficiently. These chips manage data protocols, handle voltage level translation, and mitigate noise in data paths, enabling high-fidelity signal transfer. Their functionality extends from simple serial interfaces to sophisticated high-bandwidth interconnects that support emerging technologies like artificial intelligence, 5G, and autonomous vehicles.

As electronic systems grow more complex, the role of these semiconductors becomes increasingly critical. In automotive systems, for instance, various subsystems—ranging from infotainment units to advanced driver-assistance systems (ADAS)—need to communicate swiftly and reliably. Similarly, in consumer electronics, users demand seamless interaction between components such as cameras, displays, and storage devices. Interface and connectivity semiconductors make these interactions possible by supporting a diverse array of standards and physical media.

Furthermore, these semiconductors play a foundational role in enhancing system scalability and modularity. Designers can develop systems with swappable modules or components without sacrificing performance, thanks to well-engineered interface chips. The abstraction they provide allows manufacturers to iterate on designs without overhauling the entire architecture, thus accelerating time-to-market and reducing development costs.

Market Dynamics Driving Growth

The market for interface and connectivity semiconductors is experiencing robust growth, driven by several converging trends. First and foremost is the explosive proliferation of connected devices, from smartphones and tablets to industrial sensors and medical devices. The demand for high-speed, reliable communication in these devices has propelled investments in advanced interface technologies.

The automotive sector, in particular, represents a burgeoning opportunity. With the shift toward electric and autonomous vehicles, there is a growing need for high-bandwidth communication channels between components like LiDAR sensors, cameras, and central processing units. This trend is complemented by the increasing complexity of vehicle infotainment systems and the integration of advanced navigation and telematics.

Meanwhile, in the industrial space, the advent of Industry 4.0 has catalyzed a surge in machine-to-machine communication. Factories are evolving into smart manufacturing hubs, requiring resilient and fast communication among robots, controllers, and cloud-based analytics platforms. Interface and connectivity semiconductors serve as the glue that holds these complex networks together, ensuring that data flows securely and efficiently.

Technological Innovations and Trends

The evolution of interface and connectivity semiconductors is marked by significant technological advancements aimed at overcoming traditional limitations. One of the key trends is the miniaturization of components. As devices become more compact, there is a need for smaller semiconductor packages that can still handle high data rates and power requirements. Innovations in 3D stacking and system-in-package (SiP) designs are addressing these needs effectively.

Another important trend is the integration of multiple interface standards within a single chip. Multi-protocol transceivers reduce the number of components required, simplifying board layout and reducing power consumption. This is particularly beneficial in space-constrained applications such as wearables and mobile devices. Furthermore, advances in signal conditioning, such as equalization and pre-emphasis, are enhancing signal integrity over long and noisy channels.

Power efficiency is also a growing concern, particularly in battery-operated and environmentally sensitive applications. Engineers are developing interface semiconductors that consume less power without compromising performance. These improvements contribute to longer device lifespans and lower environmental impact. As a result, sustainability has become an increasingly important design consideration in the semiconductor industry.

Challenges in Development and Deployment

Despite the exciting growth prospects, the development and deployment of interface and connectivity semiconductors come with a host of challenges. One of the primary hurdles is ensuring compatibility with a wide range of industry standards and legacy systems. Manufacturers must strike a balance between supporting new protocols and maintaining backward compatibility, which often requires complex design strategies.

Signal integrity is another critical challenge, especially as data rates increase. As frequencies rise, the susceptibility to noise, crosstalk, and electromagnetic interference also grows. This necessitates meticulous engineering of both the semiconductor and the surrounding PCB layout to maintain performance. Additionally, thermal management becomes a more pressing concern as power densities increase.

Supply chain constraints can also impede the rapid deployment of new interface technologies. Global disruptions, such as those seen during the COVID-19 pandemic, have highlighted the vulnerabilities in semiconductor manufacturing and logistics. Ensuring a stable supply chain, therefore, becomes essential for meeting market demand and maintaining product timelines.

Competitive Landscape and Key Players

The interface and connectivity semiconductor market is highly competitive, featuring a mix of established players and innovative startups. Leading semiconductor manufacturers have leveraged their scale and R&D capabilities to develop cutting-edge solutions that cater to a broad range of applications. These include companies known for their leadership in high-speed data interfaces, power-efficient transceivers, and robust physical layer implementations.

In addition to large corporations, a growing number of specialized firms are focusing on niche applications such as automotive Ethernet, USB-C, and industrial fieldbus systems. These companies often bring innovative approaches and agility to the market, helping to drive technological progress. Strategic partnerships, mergers, and acquisitions are common as companies look to expand their capabilities and market reach.

Collaborative efforts with industry standards bodies also play a vital role. By participating in the development of new interface specifications, companies can influence the direction of technology and ensure that their products align with future market needs. This collaborative model fosters innovation while ensuring a level of interoperability that benefits the broader ecosystem.

Regulatory and Standardization Factors

The development and deployment of interface and connectivity semiconductors are heavily influenced by regulatory and standardization considerations. Industry standards ensure that devices from different manufacturers can interoperate effectively, which is crucial for fostering market adoption. Organizations such as the IEEE, USB-IF, and MIPI Alliance play central roles in defining and maintaining these standards.

Compliance with electromagnetic compatibility (EMC) and safety regulations is mandatory for products intended for use in consumer, automotive, and industrial environments. These regulations vary by region, necessitating a thorough understanding of global compliance requirements during the design phase. Failure to meet these standards can result in costly redesigns, delays, and market access restrictions.

Environmental regulations, such as those related to hazardous substances and energy efficiency, further shape the design and manufacturing of semiconductors. Manufacturers must adopt sustainable practices and materials to comply with regulations like RoHS and REACH. These requirements are not just legal obligations but also key factors in building trust with environmentally conscious consumers and clients.

Strategic Opportunities Ahead

Several strategic opportunities are emerging within the interface and connectivity semiconductor space. One of the most promising areas is the continued integration of artificial intelligence (AI) and edge computing. These technologies demand rapid and reliable data transfer, which opens up new use cases for high-performance interface chips.

The transition to electric and autonomous vehicles also presents significant opportunities. Modern vehicles are becoming data centers on wheels, requiring robust and high-speed connections between sensors, processors, and control units. The adoption of MIPI A-PHY as a standardized communication protocol for automotive applications highlights the growing need for specialized interface solutions.

In the realm of industrial automation, the move toward decentralized control and real-time analytics necessitates low-latency, high-reliability communication links. Interface semiconductors designed for deterministic networking and time-sensitive applications will play a crucial role in enabling the smart factory of the future.

Navigating Market Complexities

Entering the interface semiconductor market requires a nuanced understanding of application-specific requirements, customer expectations, and competitive dynamics. OEMs and system integrators seek partners who can deliver not just chips, but comprehensive solutions that address performance, reliability, and scalability. This has led to a rise in value-added services, including design support, custom firmware, and system-level validation.

Design cycles are becoming shorter, and time-to-market pressures are intensifying. Companies must invest in simulation tools, prototyping platforms, and agile development practices to stay ahead. Additionally, customer engagement models are shifting toward co-development and joint innovation, particularly in high-stakes markets like automotive and aerospace.

Building strong customer relationships and offering differentiated value are key to thriving in this environment. Companies that can demonstrate deep application expertise and provide tailored solutions will have a competitive edge. This customer-centric approach aligns well with the strategies of leading OEM Semiconductor providers who prioritize integration, performance, and longevity.

The Future of Connectivity Semiconductors

Looking forward, the interface and connectivity semiconductor industry is poised for transformative change. Innovations in materials, such as the use of gallium nitride (GaN) and silicon carbide (SiC), promise higher efficiency and better thermal performance. These materials are particularly valuable in high-power and high-frequency applications.

Quantum computing, although still in its infancy, represents another frontier. The ultra-sensitive nature of quantum bits will necessitate entirely new paradigms of data interfacing and signal integrity. Early research and prototyping in this area suggest that interface technologies will need to evolve rapidly to meet future demands.

Interdisciplinary collaboration will be critical in shaping the next generation of connectivity solutions. Cross-functional teams involving materials scientists, electrical engineers, software developers, and system architects will drive innovation. As the industry moves forward, the ability to integrate and optimize at both the chip and system level will determine long-term success.

Conclusion

Interface and connectivity semiconductors are more than just components—they are enablers of modern digital life. From smart homes and connected cars to automated factories and cloud computing, the need for fast, reliable data communication is ubiquitous. The industry is brimming with potential, shaped by emerging technologies, evolving standards, and a relentless demand for performance.

As the ecosystem grows more interconnected, the importance of these semiconductors will only intensify. Solutions like the Interface & Connectivity Semiconductors platform are paving the way for scalable, high-performance architectures. Those who can navigate the complexities of design, regulation, and market dynamics will be well-positioned to lead in this dynamic and essential sector.

0 notes

Text

How Can AI Software Development Services Boost Your Business?

In today's rapidly evolving digital economy, staying competitive requires more than just adapting to technology—it demands innovation driven by intelligence. Artificial Intelligence (AI) is no longer a futuristic concept; it's a present-day force transforming industries across the globe. For businesses aiming to thrive in this landscape, AI software development services have emerged as a powerful catalyst for growth, efficiency, and innovation.

What Are AI Software Development Services?

AI software development services refer to the design, development, and deployment of AI-driven applications and systems tailored to specific business needs. These services often include machine learning (ML), natural language processing (NLP), computer vision, predictive analytics, and robotic process automation (RPA), among others. Leading AI development companies build intelligent systems that can learn from data, make decisions, and automate processes to drive value.

1. Streamlining Operations Through Automation

AI excels at automating repetitive and rule-based tasks. By integrating AI into core workflows, businesses can significantly reduce the need for manual intervention, minimize errors, and increase overall efficiency.

AI-powered bots can handle customer inquiries 24/7.

Intelligent automation tools can manage data entry, invoice processing, and inventory management.

Robotic Process Automation (RPA) can streamline back-office operations.

This results in cost savings, faster turnaround times, and more consistent outcomes.

2. Improving Decision-Making with Data Insights

Every business generates vast amounts of data, but only a few know how to utilize it effectively. AI software development services help transform raw data into actionable insights.

Predictive analytics models forecast trends and customer behavior.

AI algorithms identify patterns and anomalies in large datasets.

Real-time dashboards offer instant visibility into key performance metrics.

With AI, decision-makers can make more informed, data-driven choices that boost productivity and profitability.

3. Enhancing Customer Experience

Modern consumers expect personalized, seamless, and responsive interactions. AI enables businesses to deliver on these expectations:

AI chatbots offer instant customer support and query resolution.

Recommendation engines suggest products/services based on user behavior.

Sentiment analysis helps understand customer feedback in real time.

These solutions not only enhance user satisfaction but also foster customer loyalty and long-term engagement.

4. Enabling Scalable and Flexible Solutions

AI systems are inherently scalable. Whether you're a startup or an enterprise, AI solutions can grow with your business:

Cloud-based AI platforms offer flexibility and on-demand scaling.

Modular AI systems allow businesses to expand functionalities as needed.

Custom AI applications can be tailored for industry-specific use cases.

This adaptability ensures your business is always equipped to meet changing demands.

5. Strengthening Security and Compliance

Security threats and regulatory pressures continue to rise. AI can help organizations safeguard their data and ensure compliance:

AI-driven security systems detect unusual behavior and potential breaches.

Compliance automation tools help track and report regulatory adherence.

Machine learning models improve fraud detection in real-time.

These proactive security measures protect business integrity and customer trust.

6. Fostering Innovation and Competitive Advantage

AI empowers companies to innovate faster:

AI tools help in product development by analyzing user needs and testing variations.

Businesses can explore new markets with AI-powered market research.

AI accelerates R&D by simulating outcomes and optimizing processes.

Early adopters of AI not only keep up with competitors—they lead the market with smarter, faster innovations.

Conclusion

From operational efficiency and customer satisfaction to data-driven strategies and security, AI software development services offer immense value across every facet of a business. The integration of intelligent technology isn’t just a tech upgrade—it’s a strategic shift toward a more agile, innovative, and future-ready enterprise.

If you’re looking to unlock new growth opportunities, investing in AI software development services is one of the smartest business moves you can make today.

0 notes

Text

Surgical Booms Market Overview: Current Trends and Future Outlook

The Surgical Booms Market has become an integral part of modern operating rooms, reflecting the healthcare sector's growing emphasis on efficiency, safety, and technological integration. Surgical booms—ceiling-mounted arms designed to hold medical equipment, lights, gas lines, and electrical outlets—are revolutionizing the way surgical teams interact with critical infrastructure during procedures. This article explores the current trends driving the market, its evolving landscape, and what the future holds for this essential component of hospital design and surgical care.

Current Market Trends

1. Adoption of Modular and Customizable Designs

One of the most prominent trends in the Surgical Booms Market is the increasing preference for modular designs. Hospitals are moving away from one-size-fits-all solutions and opting for booms that can be customized based on surgical specialties, room size, and workflow needs. Modular booms provide greater flexibility and enable healthcare providers to future-proof their operating rooms against technological changes.

2. Integration with Advanced Surgical Technologies

Surgical booms are being designed to accommodate sophisticated technologies like high-definition monitors, endoscopy equipment, and robotic surgery systems. This integration enhances intraoperative visualization and improves surgical precision, particularly in minimally invasive and complex procedures.

3. Focus on Infection Control and Safety

With the heightened focus on hygiene and infection control—especially post-COVID—surgical booms are being designed using antimicrobial coatings and materials that are easy to clean. Additionally, the ergonomic layout provided by ceiling-mounted systems reduces floor clutter, minimizing trip hazards and contamination risks.

4. Growth in Hybrid Operating Rooms

The rise of hybrid operating rooms that combine traditional surgery with advanced imaging capabilities has led to increased demand for versatile surgical booms. These hybrid setups require booms capable of supporting both diagnostic and surgical tools, ensuring seamless coordination between surgical and imaging teams.

Market Drivers

Rising Surgical Volumes: A growing number of surgical procedures globally is a direct catalyst for the demand in the Surgical Booms Market.

Hospital Infrastructure Modernization: Many healthcare systems are investing in upgrading their facilities, which includes equipping ORs with modern booms.

Surge in Minimally Invasive Surgeries: As these surgeries rely heavily on visualization and technology, the role of surgical booms becomes even more significant.

Key Restraints

Despite the growth potential, the market does face several challenges:

High Installation Costs: Surgical booms involve a significant upfront investment, including equipment costs and structural modifications.

Maintenance Complexity: Regular servicing and technical upkeep are essential, which may deter smaller hospitals from widespread adoption.

Regional Trends

North America remains the dominant market due to advanced healthcare infrastructure and a high number of surgical procedures.

Europe is also a significant contributor, especially in countries like Germany, the UK, and France, where healthcare systems emphasize quality and innovation.

Asia-Pacific is emerging rapidly, driven by rising healthcare investments in countries such as China and India.

Latin America and Africa are gradually adopting surgical booms, primarily in private sector hospitals and international-funded healthcare initiatives.

Future Outlook

The future of the Surgical Booms Market looks promising, with several developments likely to shape its trajectory over the next decade:

Smart Booms: Integration with the Internet of Things (IoT) will enable real-time monitoring, predictive maintenance, and data analytics for improved operational efficiency.

AI Compatibility: Booms that support artificial intelligence-driven tools and robotic surgery will become increasingly important.

Green Initiatives: Energy-efficient and sustainable boom systems will gain popularity as hospitals strive for environmental compliance.

Furthermore, the growing demand for telemedicine and remote surgeries may also influence the design and functionality of surgical booms, pushing manufacturers to innovate further.

Conclusion